EMI × Kohler · Marketplace Intelligence

Kohler SEA Regional

Home & Living Marketplace Review

Indonesia · Singapore · Thailand — 12-month rolling to April 2026

An executive synthesis of Kohler's regional commercial position across Shopee, Lazada and Tokopedia — category structure, competitive standing, where the region wins and loses, channel quality, pricing and the action plan. Every figure is drawn from EMI's regional deck and is click-to-source. Figures are MAT / 12-month-rolling unless marked; the deck reports a single normalised value column, so shares (%) carry the comparison and absolute sales read as plain normalised units.

Executive Summary · Regional Market · Competitive Set · Win / Lose by Market · Growth vs Market · Channel Quality · Pricing · Hero Products · Action Plan · Sources

01 · Executive Summary

The six things to know

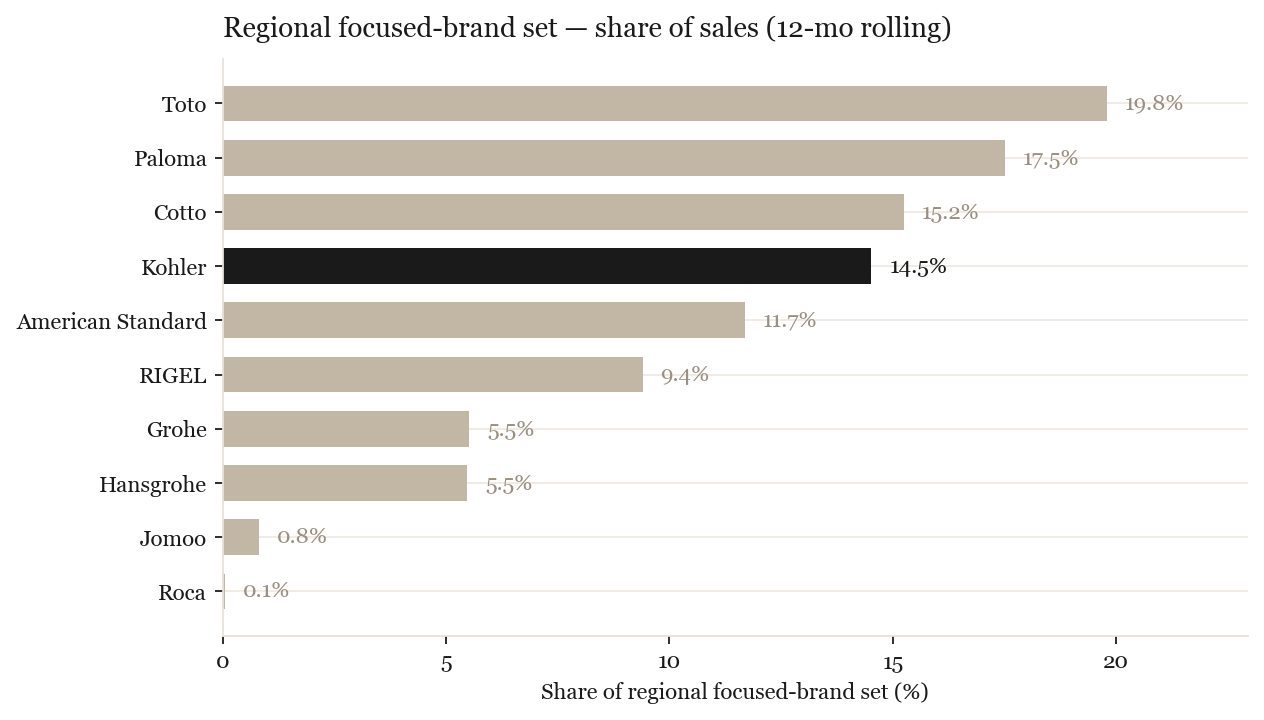

- Kohler is the region's #4 premium bathroom brand at 14.5% of the tracked focused-brand set, behind Toto (19.8%), Paloma (17.5%) and Cotto (15.3%) — a close, crowded top tier. source

- The position is highly uneven by market: Kohler is #2 in Thailand (27.2%), #3 in Indonesia (9.3%) and only #5 in Singapore (8.9%). It is the most balanced regional player but is #1 in no single market. source

- Kohler is growing fast — +46% MAT year-on-year — but Hansgrohe (+94%), RIGEL (+84%) and Cotto (+48%) are growing faster, so the top-tier order is still in play. source

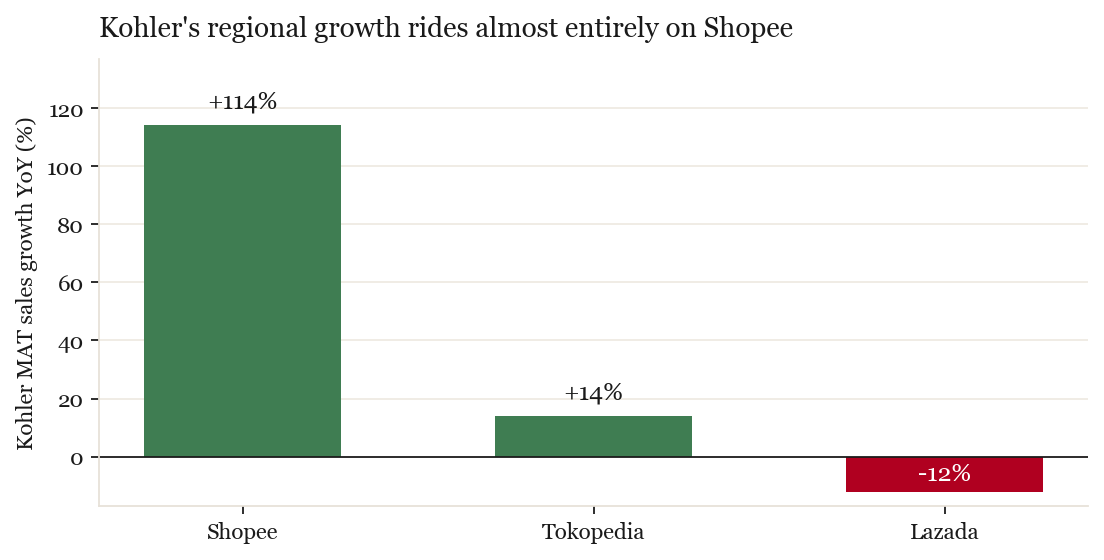

- That growth rides almost entirely on Shopee (+114% MAT), while Tokopedia is modest (+14%) and Lazada is shrinking (−12%) — a concentration risk. source

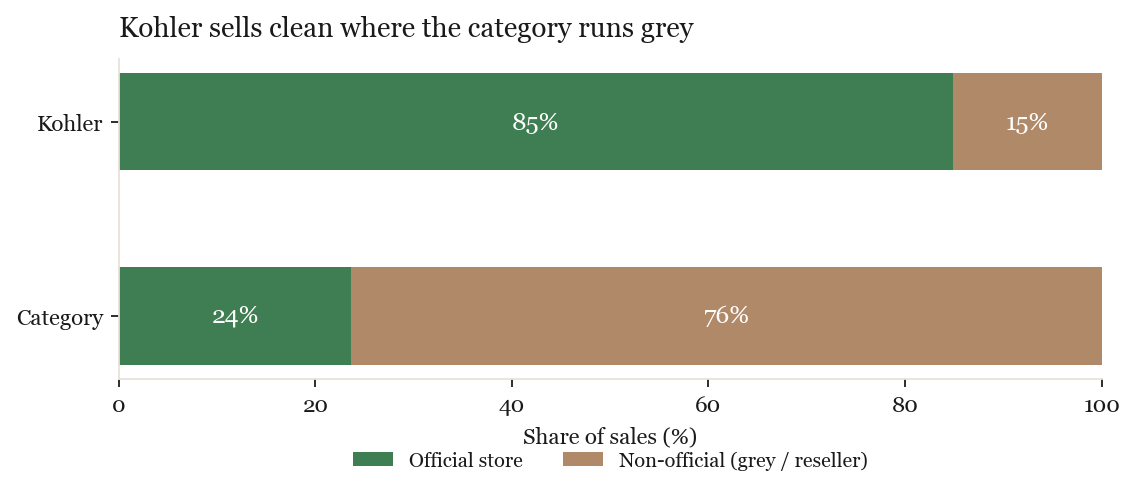

- Channel quality is Kohler's structural edge: ~85% of its sales run through official stores versus ~24% for the category, and in official-only stores Kohler ranks #2. source official rank

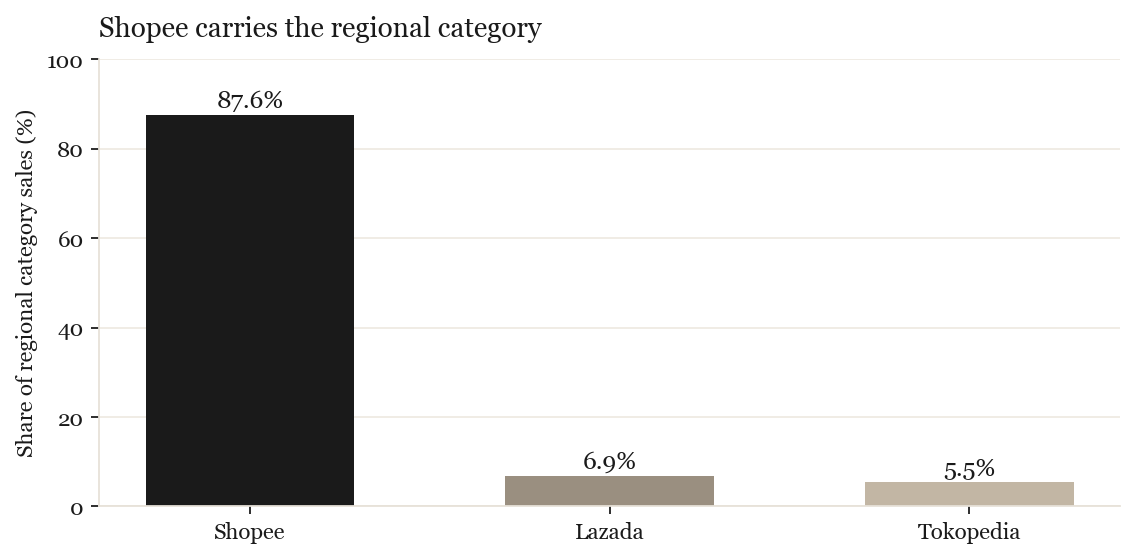

- The regional category is Shopee-dominated (87.6%) and grey-market-heavy (62%) — a value-driven marketplace where premium sanitaryware is a thin, niche slice against cheap accessories. source deck

02 · The Regional Market

A Shopee-led, grey-market category

The SEA Home & Living category EMI tracks across the three markets is large but unbranded at its core — and overwhelmingly transacted on one platform.

Platform mix differs by market: Indonesia runs on Shopee + Tokopedia; Singapore and Thailand on Shopee + Lazada. Shopee is the common spine across all three. source deck: overview

The category is dominated by unbranded, grey-channel volume

Of the 226.98M in tracked category sales, 62% flows through grey sellers and only 24% through official stores (14% resellers). The ten tracked premium brands together account for just 32.97M — about one-seventh of the category; the rest is unbranded and value-tier. The headline contest for Kohler is therefore not "share of category" but share of a small, premium, branded pocket sitting on top of a vast value market. source deck: focused brands

03 · The Focused-Brand Competitive Set

A crowded premium top tier

Within the tracked premium set (32.97M, 12-month rolling), Kohler sits fourth — inside four share points of the #1 position, but with two single-market leaders ahead of it.

| # | Brand | Regional sales | Share | Footprint |

|---|---|---|---|---|

| 1 | Toto | 6.52M | 19.8% | Regional (ID-led) |

| 2 | Paloma | 5.77M | 17.5% | Indonesia only |

| 3 | Cotto | 5.03M | 15.3% | Thailand only |

| 4 | Kohler | 4.79M | 14.5% | Regional (all 3) |

| 5 | American Standard | 3.85M | 11.7% | Regional (all 3) |

| 6 | RIGEL | 3.10M | 9.4% | Singapore only |

| 7 | Grohe | 1.82M | 5.5% | Regional (SG-led) |

| 8 | Hansgrohe | 1.80M | 5.5% | Singapore-led |

| 9 | Jomoo | 0.27M | 0.8% | Singapore-led |

| 10 | Roca | 0.02M | 0.1% | ID + TH |

The crucial structural read: the two brands ahead of Kohler win by dominating a single home market — Paloma is essentially all-Indonesia, Cotto all-Thailand. Kohler, American Standard and Toto are the only genuinely tri-market brands. Kohler's regional rank understates a real strength — it competes everywhere — but also flags the gap: it leads nowhere. source deck

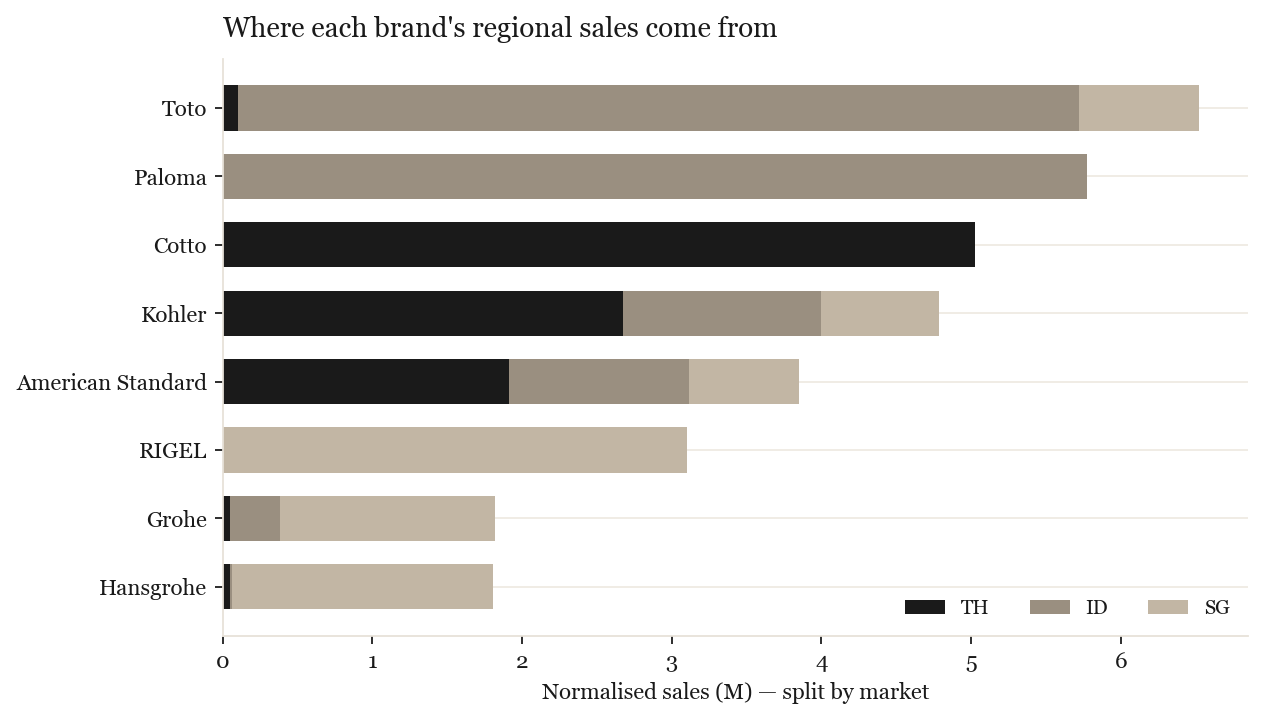

04 · Where Kohler Wins and Loses

One stronghold, one mid-pack, one weak spot

Read as a portfolio, Kohler's regional 14.5% is the blend of three very different stories.

Thailand — the stronghold

Kohler is the clear #2 at 27.2%, behind only Cotto's ceramic juggernaut (51%) and ahead of American Standard (19.5%). At 2.67M, Thailand is comfortably Kohler's largest regional market and its profit engine. source

Indonesia — mid-pack behind two giants

Kohler is #3 at 9.3%, but a distant third: Paloma (40%) and Toto (39%) together own ~80% of the premium set. Indonesia is also where Kohler's channel is leakiest — external research flags persistent structural counterfeiting and unauthorised selling on Indonesian marketplaces (see Channel Quality). source EXT ↗ counterfeiting

Singapore — the weak spot

Kohler is only #5 at 8.9%, in a premium-skewed market led by RIGEL (35%), Hansgrohe (20%) and Grohe (16%), with Toto (9%) also ahead. Singapore is the clearest underperformance relative to Kohler's global brand strength. source External research suggests the online #5 is a downstream symptom: premium demand in Singapore is set in the offline interior-designer / trade channel, where Hansgrohe is entrenched — Kohler under-indexes where the specification decision is actually made. EXT ↗ designer channel EXT ↗

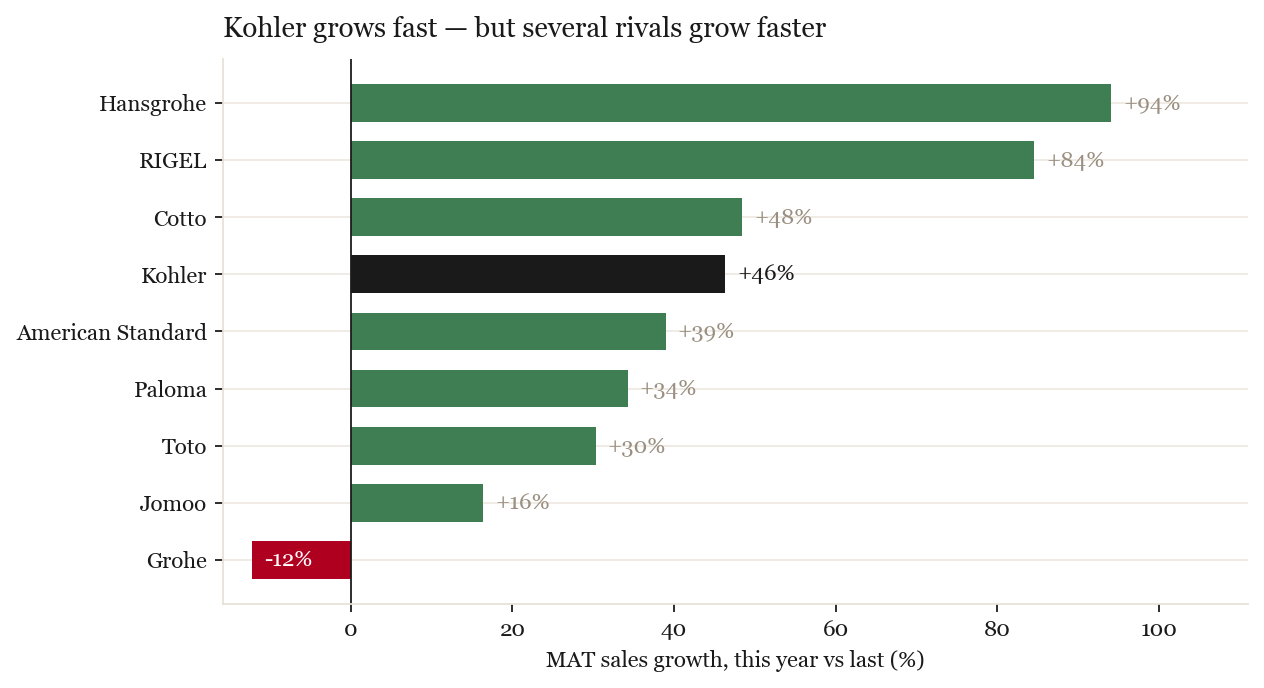

05 · Growth vs the Market

Fast — but several rivals are faster

On a moving-annual basis Kohler is growing strongly, but the brands closing on its position are growing faster, and its growth is dangerously concentrated on one platform.

Kohler grew +46% MAT year-on-year — top-tier momentum — but Hansgrohe (+94%), RIGEL (+84%) and Cotto (+48%) all grew faster, while Grohe (−12%) is the only top brand shrinking. The premium pecking order is therefore not settled. source deck

Read with care: the category's reported +123% MAT is lifted by a +176% step-change in Shopee's tracked sales — partly a coverage effect — so the brand-level growth rates above are the cleaner signal. Likewise, single-month April momentum (Kohler −27% MoM in the deck) is volatile and is not used for ranking here. deck: April momentum

Growth concentration: the Shopee dependency

Kohler's regional growth is almost entirely a Shopee story (+114% MAT). Tokopedia adds a modest +14% and Lazada is contracting (−12%). A single-platform growth engine is fragile — a Shopee algorithm shift or fee change would hit Kohler disproportionately. source

External signal · the platform map is shifting under this

Regional e-commerce GMV hit US$157.6bn in 2025 (Shopee ~53%), but the growth has moved: TikTok Shop GMV grew +66% to ~31% of platform GMV, while Lazada fell −28% — rebuilding around a brand-led LazMall. At the same time Shopee added a 5% technical-support fee, pushing premium take-rate past 15%. The economics now favour high-AOV products sold through live commerce (5–7% conversion vs ~1–2% for static listings; trusted niche influencers convert up to 82%). The read for Kohler: don't just defend Shopee — deliberately build TikTok Shop as a discovery engine and LazMall as the authenticity boutique. EXT ↗ SEA GMV EXT ↗ TikTok +66% EXT ↗ Shopee fees EXT ↗ live commerce EXT ↗ LazMall06 · Channel Quality

Kohler sells clean where the category runs grey

Kohler's strongest and most defensible regional asset is the quality of its channel mix.

~85% of Kohler's regional sales run through official stores, against just ~24% for the category as a whole (which is 62% grey, 14% reseller). This is the cleanest channel position in the premium set and a genuine moat: official-store sales protect price, warranty and brand experience in a marketplace built on grey supply. source deck

The moat shows up in the rankings: filter to official stores only and Kohler climbs to #2 (19.2%) from #4 overall — ahead of RIGEL, Cotto and Toto, behind only Paloma. Kohler is structurally stronger exactly where buyers trust the channel. source deck

External signal · how to harden the moat

Two mechanisms surface from the research. First, destroy the grey market's utility: gate digital warranty activation, software updates and certified installation behind a verified Official-store invoice — a service layer resellers can't replicate. EXT ↗ warranty walls Second, widen the top of the funnel with a consumable wedge: a proprietary shower filter on a recurring-cartridge subscription (a market growing ~8.4% CAGR) recruits younger buyers, guarantees recurring revenue, and pulls customer data off the anonymous marketplace into Kohler's CRM. EXT ↗ filter market EXT ↗ subscription model07 · Pricing & Segmentation

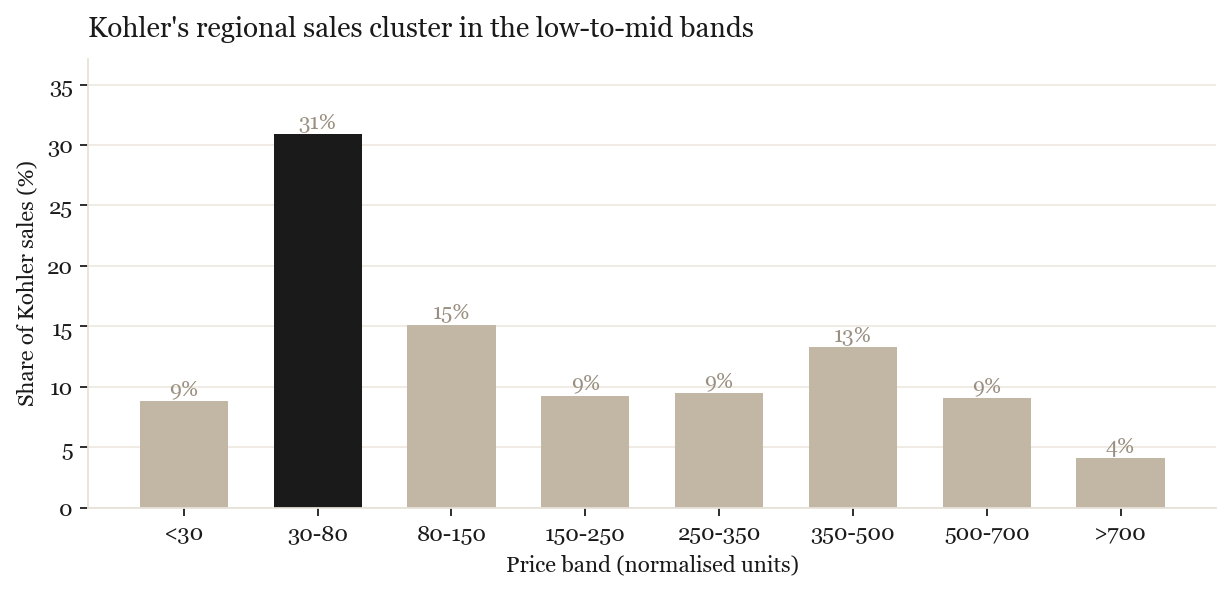

Anchored low-to-mid, with a premium shoulder

Kohler's regional sales concentrate in the accessible bands, with a distinct secondary peak in the upper-mid tier — the premium shoulder where the brand earns its margin.

Almost a third of Kohler's regional sales (31%) sit in the 30–80 band, with a further 15% at 80–150 — accessible price points that drive unit volume (handshowers, sprays, accessories). But a clear secondary peak at 350–500 (13%) plus 9% at 500–700 shows Kohler also converts genuine premium demand. Its average selling price (~124 normalised) is roughly 8× the category average (~15) — Kohler competes on value per unit, not volume. source deck: vs field

08 · Hero Products

Premium is niche against cheap-accessory volume

The regional best-seller list is a useful reality check on where marketplace volume actually sits — and it is not in premium sanitaryware.

The regional top-20 by sales (official stores) is the raw, unfiltered Home & Living category — dominated by low-price, off-category and local listings: spring mattresses, shower-head water filters, ceramic toilets and the like, mostly under a few hundred normalised units each. Premium bathroom brands barely register at the unit-volume top of the market. deck: top 20

Kohler's marquee entries

Kohler's only appearances in the regional official top-20 are the Aparu 3-way thermostatic shower column (K-37963T) and the Watermind round handshower (K-R28694T) — showering products, not ceramics. This is consistent with the pricing read: Kohler wins on value per unit (high ASP), not on appearing in a volume chart led by sub-30 accessories. The strategic takeaway is that a pure best-seller-chasing play is the wrong game for a premium brand here; the win is premium showering and smart fixtures, sold clean through official stores. source

09 · AI Action Plan

Eleven regional priorities

Turning the regional read into moves — first-party priorities sharpened with an external-context layer (Aissistance Deep Research), and several new plays the research surfaced, from an after-sales moat to a prefab-bathroom B2B channel and the region's ageing-population shift.

1 · Defend Thailand

Protect the #2 / 27% franchise via showers, thermostatics & smart fixtures — not a ceramic-volume war with Cotto.5 · Fortify the Official moat

Gate warranty, updates & certified install behind Official-store invoices — a service layer resellers can't copy.9 · Build an after-sales moat

Local repair networks & subsidised legacy parts — close the spare-parts gap TOTO exploits.2 · Win Singapore's trade channel

Attack the interior-designer / specification ecosystem where Hansgrohe is entrenched — not just the listing.3 · Reclaim Indonesia's grey leakage

Warranty-registration walls that destroy the utility of unauthorised stock.4 · De-risk beyond Shopee

Stand up TikTok Shop (+66% GMV) as discovery; LazMall as the authenticity boutique.10 · Open the prefab (PBU) channel

Lock exclusive supply contracts with prefab-bathroom integrators — fixtures specified before ground breaks.7 · Sell a wellness ecosystem

Reframe Anthem/Statement as hydrotherapy systems — countering TOTO WASHLET & GROHE SPA on experience, not spec.8 · Weaponise smart retrofits

Easy-install bidet seats & shower panels sold direct via live commerce — capture upgrades without contractors.6 · Consumable wedge

A shower-filter subscription to acquire younger buyers, bank recurring revenue and own the CRM.11 · Design for the Silver Economy

Universal-design premium fixtures for a fast-ageing region (Thailand 28% elderly by 2033).- Defend Thailand as the profit engine. Kohler's #2 / 27% Thai position is its single biggest regional asset. With the Thai economy stagnant (~0.9% GDP) and new builds soft, do not chase Cotto's ceramic volume; instead own the high-margin smart-retrofit space — premium bathroom imports are still growing ~11.9%. source EXT ↗ Thai economy EXT ↗ premium imports

- Fix Singapore by winning the trade channel. The online #5 is downstream of the offline interior-designer ecosystem, where Hansgrohe is entrenched. The sharp wedge is a dedicated B2B2C trade programme for top design firms — marketing concealed, space-saving fixtures (HDB constraints) and hero digital showers — not a broad consumer push. source EXT ↗ designer channel

- Grow Indonesia by recovering grey leakage. Kohler is #3 behind two giants owning ~80%, in its leakiest channel. Rather than conquest Paloma/Toto head-on, deploy strict digital warranty registration walls requiring an Official-store invoice — instantly destroying the post-purchase value of grey stock. source EXT ↗ warranty walls

- De-risk the platform mix. +114% Shopee against −12% Lazada makes the engine single-threaded. The regional growth has moved to TikTok Shop (+66%); launch it now as a top-of-funnel discovery channel using design micro-influencers (live commerce converts at 5–7%), while keeping LazMall as the authenticity boutique. source EXT ↗ TikTok EXT ↗ live commerce

- Fortify the official-store moat. 85% official versus a 62%-grey category is Kohler's structural edge. Bundle exclusive online-only SKUs with certified installation and maintenance available only through Official stores — a service barrier no reseller can match. source EXT ↗ service moat

- Widen the funnel with a consumable wedge. Beyond Kohler's accessible-band demand (31% of sales at 30–80), launch a high-design shower filter on a recurring subscription — a market growing ~8.4% CAGR — to recruit younger buyers, bank predictable revenue and pull data into Kohler's CRM. source EXT ↗ filter market EXT ↗ subscription

- Pivot to a "wellness ecosystem" narrative. To bypass the volume fortresses of single-market incumbents, stop selling fixtures and sell systems — position Anthem and Statement as tech-enabled hydrotherapy/wellness experiences, matching TOTO's WASHLET and GROHE's "SPA" plays and shifting the contest to experiential luxury that justifies premium price. EXT ↗ wellness systems EXT ↗ GROHE SPA EXT ↗ TOTO WASHLET

- Weaponise smart retrofits across the region. Capitalise on upgrades that bypass full renovation: market easy-install smart bidet seats and premium shower panels direct to homeowners via e-commerce and live commerce. Kohler's Numi wins on wow-factor (TOTO leads on reliability) — so lead with design and experience for the untapped retrofit segment. EXT ↗ smart retrofit EXT ↗ flagship head-to-head

- Build a spare-parts and after-sales moat. Ground-level forums show SEA buyers weigh ease of finding spare parts as heavily as features — and TOTO's local Saraburi plant gives it cheap, fast replacement modules, while Kohler's post-warranty electronic parts can be prohibitively expensive. Decouple servicing from third-party distributors, stand up responsive local repair networks and subsidise legacy components, so lifetime cost of ownership protects loyalty rather than eroding it. This directly neutralises a structural TOTO advantage. EXT ↗ spare-parts EXT ↗ post-warranty cost

- Open the prefabricated-bathroom (PBU) B2B channel. Prefab bathroom pods are now specified in ~63% of new hotels over 150 rooms (and over half of senior-living projects); fixtures are chosen at the factory-integrator stage, long before a developer is pitched. Secure exclusive, standardised supply contracts with PBU integrators so Kohler is designed-in to assembly-line bathrooms across the region's hospitality and institutional pipeline — a channel entirely separate from the marketplace. EXT ↗ prefab bathroom units

- Productise for the Silver Economy. The region is ageing fast — Thailand reaches ~28% elderly by 2033 — and premium universal design (discreet ergonomic heights, antimicrobial glazing, slip-resistance built into flagship aesthetics, not clinical add-ons) is becoming table stakes for high-end renovations. Build an accessibility-grade tier that reads as luxury, ahead of the demographic curve. EXT ↗ ageing society

External signal · on the 5-year horizon

Two further shifts to watch (and pilot early): the med-tech convergence — smart toilets becoming passive health-diagnostic hubs, opening a hyper-premium tier (HK$18k–45k+) that needs wellness/clinical go-to-market, not hardware retail; and an analog counter-movement at the top — "digital fatigue" reviving solid-brass, PVD-coated, tactile fixtures, where the margin lies in metallurgy and finish durability rather than connectivity. EXT ↗ diagnostic toilets EXT ↗ analog luxury10 · Sources

Every insight, traced

Click any insight's “source” tag above, or any thumbnail below, to view the underlying chart or deck slide. Derived charts are computed from the figures in the EMI × Kohler SEA Regional deck (12-month rolling / MAT to April 2026, across Shopee, Lazada and Tokopedia); deck pages are reproduced as click-to-source evidence. Insights marked EXT ↗ draw on a separate external-research layer, cited below and kept distinct from the first-party EMI data.

External research

Aissistance Deep Research, 3-pass run (June 2026). Each item below links out to the cited public source in a new tab; findings are folded into the Action Plan and outlook as a clearly-labelled context layer, separate from the first-party marketplace data.